Law Enforcement Officers’ Pension System

Deferred Retirement Option Program (DROP)

Enrollment Package

This package contains

A Summary of DROP

Application for Retirement (Form 98-101)

Special Tax Notice Regarding Your Rollover Options

Application for DROP (Form 504)

Binding Letter of Resignation (Form 507)

Please note the following

You must send proof of birth for your beneficiary with this application.

Your application must be received prior to the first of the month in which

you wish to enroll in DROP.

Deferred Retirement

Option Program

This page intentionally left blank

Page 2 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

While in DROP, a State participant is subject to the personnel law, regulations and policies applicable to an

employee of the State. The participant continues to receive compensation, health insurance and other benefit

options established under the State employee and retiree health and welfare benefit program.

At least 25 but less than 32 years of creditable

service in the Law Enforcement Officers’ Pension System

(LEOPS).

Lesser of:

a. 7 years,

b. Difference between 32 years and the member's creditable service as of the date the member elects to

participate or

c. A term selected by the member (which may not exceed 7 years).

File a DROP enrollment packet containing the following:

a. Application for Service Retirement (Form 98),

b. Application for DROP (Form 504) and

c. Binding Letter of Resignation (Form 507)

A DROP participant is a “retiree” of the Law Enforcement Officers’ Pension System and as a retiree:

a. Does not pay any member contributions,

b. Does not accrue additional retirement service credit in LEOPS,

c. Does not derive a benefit from any increases in earnable compensation or unused sick leave,

d. Is not eligible to receive an ordinary disability retirement allowance, but may be eligible to receive an

accidental disability retirement allowance and

e. Is not subject to reemployment rules while participating in DROP.

SRA credits to the participant's DROP account:

a. Normal service retirement allowances that the participant would have received had he or she received

pension payments as of the effective date of his or her participation in the DROP,

b. Retiree cost-of-living adjustments payable when eligible and

c. Interest on the balance in the account at the rate of 4% a year, compounded annually.

SRA will provide an annual statement of the balance in the participant's DROP account at fiscal year end.

a. On the DROP termination date selected by the participant, or

b. If the employer terminates the participant's employment, or

c. If the participant terminates employment early, or

d. If the participant accepts an accidental disability retirement allowance, or

e. If the participant dies.

DROP participants are not eligible for ordinary disability retirement. DROP participants may apply for an acciden-

tal disability retirement allowance only if they are totally and permanently incapacitated for duty as a result of an

accident or condition that arises out of or in the course of the actual performance of duty during their participation

in the DROP, and without willful negligence on their part.

Payment of balance in DROP account: Upon application for withdrawal of the accumulated DROP funds, the

SRA will pay the amount accrued in the DROP account as directed. Any taxable amounts not rolled over to

another tax deferred plan will be subject to mandatory federal and Maryland state withholdings. Please refer to

the “Special Tax Notice Regarding Your Rollover Options” for important information regarding your options to

continue to defer federal income tax on your plan benefits.

Payment of LEOPS benefits: The SRA begins paying the normal service retirement allowance, increased by

any cost-of-living adjustments occurring during DROP participation. The allowance is not adjusted for any

increases in the member's earnable compensation or additional unused sick leave.

If the participant dies prior to ending DROP participation, the balance in the DROP account is paid to the partic-

ipant's surviving spouse. If not survived by a spouse, the participant's children who have not attained age 26 are

entitled to the balance in the DROP account. If the DROP participant is not survived by a spouse or minor chil-

dren, the balance in the account is payable to the designated beneficiary. SRA also begins paying the surviving

spouse 50% of the participant's normal service retirement allowance (computed as of the date of the participant's

election to participate in the DROP).

Eligibility to

Participate

Participation

Period

How to

Participate

LEOPS Benefits

During DROP

Participation

DROP Benefits

During DROP

Participation

DROP --

Accidental

Disability

Benefits

Participation

Ends

Effect of End

of DROP

Participation

DROP Death

Benefits

Other

Deferred Retirement Option Program (DROP) Summary

for Members of the Law Enforcement Officers’ Pension System

Maryland State Retirement and Pension System ● 120 E. Baltimore St., Baltimore, MD 21202-6700 ● sra.maryland.gov

Rev. 7/23

Page 3 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Deferred Retirement

Option Program

This page intentionally left blank

Page 4 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

MARYLAND STATE RETIREMENT AGENCY

120 EAST BALTIMORE STREET

BALTIMORE, MD 21202-6700

APPLICATION FOR SERVICE OR DISABILITY RETIREMENT

LAW ENFORCEMENT OFFICERS

IMPORTANT: If you are applying for disability, this form must be completed and

filed within 120 days of notification of Board approval for disability retirement.

COMAR 22.06.01.03B states that the disability retirement application is

submitted on the date that it is received at the Retirement Agency’s mailing

address. A disability form is not considered submitted if it is provided to an

employer of the applicant. Contact the Agency to confirm receipt. COMAR

17.04.03.16E also states, if a State employee is approved for disability

retirement by the Maryland State Retirement Agency, unless the employee

resigns or is removed earlier, the employee shall be considered resigned from

State service as of the 120

th

day after the approval.

RETIREMENT

USE ONLY

FORM 98-101 (REV. 5/21)

INSTRUCTIONS FOR COMPLETION OF APPLICATION

IMPORTANT: Read the following instructions and information carefully before filling out this form.

1. If you are married at time of retirement, you must choose the Basic Allowance.

2.

After you have completed this form, you should also complete Forms 85 (Direct Deposit - Electronic Funds Transfer Sign-

Up) and 766 (Federal and Maryland State Tax Withholding Request) and forward them to your Retirement Coordinator.

3. If you have chosen the Basic Allowance or payment option 2, 3, 5 or 6, you must verify your beneficiary's date of birth by

attaching a copy of his or her birth certificate, valid driver’s license or other proof. For information on acceptable proofs of

birth date, call a Retirement Benefits Specialist at the number shown below.

4. If you are electing Option 2 or 5, you cannot designate a beneficiary who is more than 10 years younger unless the

beneficiary is your disabled child. If you elect Option 2 or Option 5 and designate your disabled child, you must submit a

completed Form 143 (Verification of Retiree’s Disabled Child for Selection of Option 2/5 Beneficiary) with this application.

5. If you wish to purchase previous service or apply for military service for which you are eligible, ask your Retirement

Coordinator for the proper form(s) and submit it with this application. Additional credit cannot be claimed or purchased after

your retirement.

6. If you wish to name more than one beneficiary and you are choosing the Option 1 Allowance or the Option 4 Allowance,

you should not fill out the

ADesignation of Beneficiary@ section on page 2. Instead, fill out and attach Form 4 (Designation

of Beneficiary Form).

7. If you are eligible to participate in the State Employees Health Insurance Program, The Basic Allowance or Option 2, 3, 5 or

6 continue health program coverage for your eligible surviving dependents, after your death. Contact your employing

agency for details.

8. You may change your retirement allowance selection only by filing a change with the State Retirement Agency before your

first payment is due. In most cases, the first payment is due 30 days after the effective date of your retirement. You cannot

change your selection after this due date.

9. If you die before the effective date of your retirement, your beneficiary cannot receive a retirement allowance even if you

have completed this form. If you are still in active service at the time of your death, your beneficiary is only eligible for the

active service death benefit.

10. You may change your beneficiary at any time. Depending on the option you have chosen, however, your retirement

allowance may have to be recalculated to reflect the change. Your benefit amount could be reduced as a result of the

change. For more information, call a Retirement Benefits Specialist.

11. You must retire within 30 days of separating from employment with a participating employer to receive additional creditable

service for your unused sick leave. Unused sick leave is sick leave that was available to an employee as sick leave during

employment and was not used before retirement. Any converted leave that was not sick leave during employment may not

be reported.

12. Generally speaking, no member may receive more than one type of retirement benefit.

13. If you have voluntary contributions in your account and have elected to withdraw them in a lump sum, you must attach a

completed Application for Withdrawal of Voluntary Funds Package to this application. This package may be obtained by

calling a Retirement Benefits Specialist at the number shown below.

NEED HELP?: If you need help to complete this form, or any information on your retirement benefits or retirement process, call

a Retirement Benefits Specialist at 410-625-5555 or toll-free 1-800-492-5909.

Page 5 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Reemployment After Retirement

for Retirees of the Law Enforcement Officers’ Pension System

VIDEO: For an overview of this information, go to sra.maryland.gov, select YouTube or Vimeo and watch “Reemployment After Retirement.”

Keep a copy of this information on file as a handy reference for the future. You should also keep your Notice of Retirement

Allowance that the Retirement Agency will send to you as a new retiree. The Notice of Retirement Allowance includes

information such as the amount of your monthly retirement allowance, the beneficiary you designated and your earnings

limitation. To determine what, if any, earnings limitation applies and the effect, if any, on your retirement allowance, you need

your Notice of Retirement Allowance to identify the type of retirement you are receiving (service, ordinary disability or accidental

disability) and your earnings limitation. Then apply the reemployment rules. Reemployment earnings are the annual

reemployment compensation reported to the IRS that the retiree received during a calendar year. Note the reemployment rules

do not apply while a retiree is participating in the Deferred Retirement Option Program (DROP).

Under no circumstances should your decision to retire be conditioned upon an offer of reemployment, and in fact, no offers of

reemployment should be discussed by you and your employer prior to your retirement. However, if after your retirement you

consider reemployment with an employer that participates in the State Retirement and Pension System (SRPS) you need to be

aware of two important issues: Internal Revenue Service (IRS) guidelines regarding reemployment and Maryland retirement law

regarding reemployment.

INTERNAL REVENUE SERVICE GUIDELINES REGARDING REEMPLOYMENT

There can be significant consequences to you and the SRPS if you retire before the normal retirement age of your plan and/or

before age 59 1/2, and are reemployed with the same employer without a bona fide separation of service. Please note that all

units of Maryland state government, including the University System of Maryland, are considered one employer.

The IRS can impose a significant tax penalty on your income if you are under the age of 59 1/2, retire and begin receiving your

monthly retirement benefits, and are reemployed by the same employer from whom you retired. In order to avoid this penalty

there must be a bona fide separation from service between you and your former employer.

If you retire before your normal retirement age, there are also serious IRS consequences to the SRPS if a bona fide separation

does not take place following retirement and prior to reemployment with the same employer.

While the IRS has not specifically defined what constitutes a bona fide separation from service, it is clear that the more

differences between your last job before retirement and the job being performed upon your reemployment, and the longer the

break between the date of your retirement and the date of your reemployment, the more likely it is that there has been a bona

fide separation of service. If you are reemployed to perform the same job, even if there is a reduction in your work schedule, this

would not likely qualify as a bona fide separation of service unless there is a lengthy break in employment. Even arrangements

where you are rehired as an “independent contractor” may not meet the IRS’ standard.

MARYLAND RETIREMENT LAW REGARDING REEMPLOYMENT

There must be a minimum of 45 DAYS between your retirement date and the date you are rehired by any employer that is a

participating employer in the SRPS. All units of Maryland State government, including the University System of Maryland, are

considered to be one employer under these reemployment rules.

Additionally, employment after retirement, under certain conditions, may cause your retirement allowance to be reduced.

SERVICE RETIREMENT

There is no earnings limit regardless of your employer. Your monthly benefit allowance will not be reduced by any earnings

made after you have retired. If you are reemployed by a participating employer, you will not rejoin the system and you will not

earn service credit from your new employment.

(FOR DISABILITY RETIREMENT RULES, PLEASE SEE FOLLOWING PAGE)

I acknowledge that I have received this information about my obligation with regard to reemployment and I agree to notify the

Board of Trustees of my anticipated earnings should I return to work. I also understand that should I exceed the earnings

limitations imposed by law, my monthly retirement allowance may be reduced or terminated until such time that any resulting

overpayment of benefits is recovered. I understand that I must be separated from any and all employment, including substitute,

seasonal, temporary, contractual, and/or permanent employment, with any employer that participates in the SRPS at the date of

my retirement. By signing this form, I am certifying to the Maryland State Retirement Agency that at the date of my retirement, I

will not be employed in any capacity by any employer that participates in the SRPS and that no discussions or offers of

reemployment after my retirement have occurred between me and any employer that participates in the SRPS.

Page 6 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

DISABILITY RETIREMENT

(continued from previous page)

Suspension of Disability Retirement: An ordinary or accidental disability allowance shall be temporarily suspended if the

retiree:

● Is not eligible for normal service retirement, and

● Is employed by a participating employer as a probationary status law enforcement officer, a law enforcement officer, or

chief as defined in §3-101 of the Public Safety Article, and

● Is receiving an annual compensation that is at least equal to the retiree’s average final compensation at retirement.

There is no additional benefit accrued while employed. If suspended, the retiree’s allowance will be reinstated on the first day of

the month following the month in which the retiree ceased employment with the participating employer. The retiree’s allowance

at time of reinstatement will be adjusted to reflect the accumulated cost-of-living adjustments during suspension. Please note

that the temporary suspension of a disability benefit causes the temporary suspension of retiree health insurance coverage if a

deduction was being made from your monthly benefit for this coverage.

Earnings Limitation for Ordinary Disability Retirees Only: A retiree receiving an ordinary disability allowance shall be subject

to an earnings limitation if the retiree:

● Is under normal retirement age, and

● Is employed by a participating employer as a probationary status law enforcement officer, a law enforcement officer, or

chief as defined in §3-101 of the Public Safety Article, and

● Is receiving an annual compensation that exceeds the retiree’s earnings limitation.

The reduction will be $1 for every $2 earned in excess of the limit, if you have been retired less than 10 years. If you have been

retired 10 years or longer, the reduction will be $1 for every $5 over the limit.

An earnings limitation does not apply for Accidental Disability Retirees.

If you have any questions, call a retirement benefits specialist at 410-625-5555 or toll free 1-800-492-5909 to understand how

the reemployment provisions apply to you. We will make every effort to assist you in understanding your options, but it is your

responsibility to advise us of your reemployment.

Page 7 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

PARTICIPATING EMPLOYERS *

Maryland State Retirement and Pension System

State of Maryland

University System of Maryland

Baltimore City and All County Boards of Education (Teachers’ System)

Community Colleges and All Public Libraries (Teachers’ System)

Participating Governmental Units in the Employees’ System as of July 1, 2017

Allegany College of Maryland

Allegany County Board of Education

Allegany County Commission

Allegany County Housing Authority

Allegany County Library

Allegany County Transit Authority

Annapolis, City of

Anne Arundel County Board of

Education

Anne Arundel County Community

College

Berlin, Town of

Berwyn Heights, Town of

Bladensburg, Town of

Bowie, City of – Police Dept. (LEOPS)

Brunswick, City of

Calvert County Board of Education

Cambridge, City of

Caroline County Board of Education

Caroline County Sheriff Deputies

Carroll County Board of Education

Carroll County Public Library

Carroll Soil Conservation District

Catoctin & Frederick Soil

Conservation District

Cecil County Board of Education

Cecil County Government

Cecil County Library

Centreville, Town of

Chesapeake Bay Commission

Chestertown, Town of

Cheverly, Town of

College of Southern Maryland

College Park, City of

Crisfield, City of

Crisfield Housing Authority

Cumberland, City of

Cumberland, City of - Police Department

Denton, Town of

District Heights, City of

Dorchester County Board of Education

Dorchester County Commission

Dorchester County Roads Board

Dorchester County Sanitary Commission

Eastern Shore Regional Library

Edmonston, Town of

Emmitsburg, City of

Federalsburg, Town of

Frederick County Board of Education

Frostburg, City of

Fruitland, City of

Garrett County Board of Education

Garrett County Community Action

Committee

Greenbelt, City of

Greensboro, Town of

Hagerstown, City of

Hagerstown Community College

Hampstead, Town of

Hancock, Town of

Harford Community College

Harford County Board of Education

Harford County Government

Harford County Library

Housing Authority of Cambridge

Howard Community College

Howard County Board of Education

Howard County Community Action

Committee

Hurlock, Town of

Hyattsville, City of

Kent County Board of Education

Kent County Commissioners

Kent Soil and Water Conservation District

Landover Hills, Town of

La Plata, Town of

Lower Shore Private Industry Council

Manchester, Town of

Maryland Health & Higher Education

Facilities Authority

Middletown, Town of

Montgomery College

Morningside, Town of

Mount Airy, Town of

Mount Rainier, City of

New Carrollton, City of

North Beach, Town of

Northeast Maryland Waste Disposal

Authority

Oakland, Town of

Oxford, Town of

Pocomoke, City of

Preston, Town of

Prince George’s Community College

Prince George’s County Board of

Education

Prince George’s County Crossing Guards

Prince George’s County Government

Prince George’s County Memorial Library

Princess Anne, Town of

Queen Anne’s County Board of Education

Queen Anne’s County Commission

Queenstown, Town of

Ridgely, Town of

Rock Hall, Town of

St. Mary’s County Board of Education

St. Mary’s County Commission

St. Mary’s County, Housing Authority

St. Mary’s County Metropolitan Commission

St. Michaels, Commissioners of

Salisbury, City of

Shore Up!

Snow Hill, Town of

Somerset County Board of Education

Somerset County Commission

Somerset County Economic Development

Commission

Somerset County Sanitary District, Inc.

Southern Maryland Tri-County

Community Action Committee

Sykesville, Town of

Takoma Park, City of

Talbot County Board of Education

Talbot County Council

Taneytown, City of

Thurmont, Town of

Tri-County Council of Western Maryland

Tri-County Council for the Lower

Eastern

Shore

University Park, Town of

Upper Marlboro, Town of

Walk

ersville, Town of

Washington County Board of Education

Washington County Board of

License Commission

Washington County Library

Westminster, City of

Worcester County Board of Education

Worcester County Commission

Wor-Wic Community College

*NOTE: The list of employers that participate in the Maryland State Retirement and Pension System (SRPS) is subject to

change at any time. This list is updated annually. To determine whether a particular employer participates in SRPS, call a

retirement benefits specialist at 410-625-5555 or toll-free at 1-800-492-5909.

Page 8 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

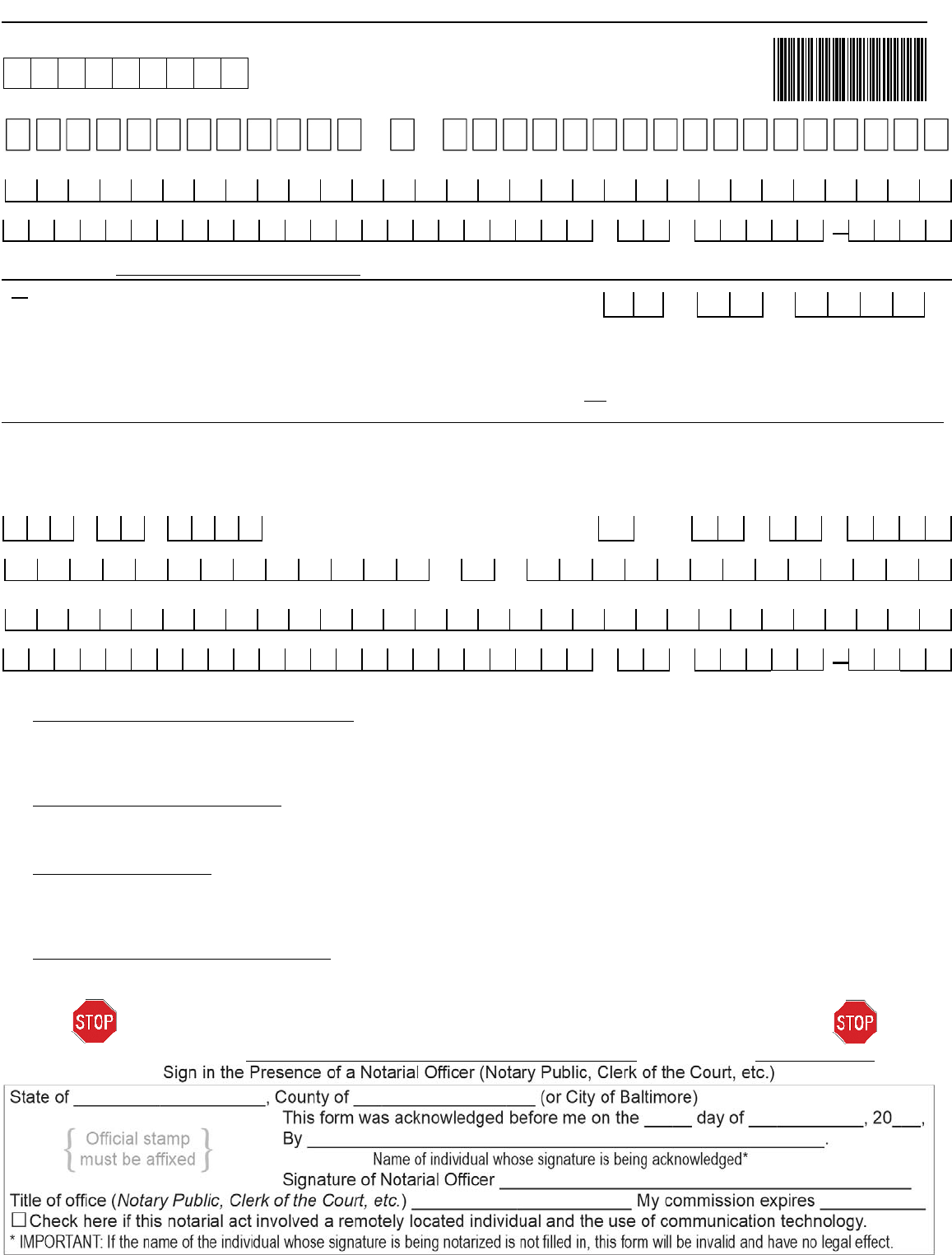

APPLYING FOR: Check only one box

□ Service Retirement

□ Ordinary Disability Retirement

□ Accidental Disability Retirement

Month Day Year

APPLICATION FOR SERVICE OR DISABILITY RETIREMENT

APPLICANT'S SOCIAL SECURITY NUMBER

APPLICANT’S NAME

First Initial Last

HOME ADDRESS

Number and Street

City State ZIP Code

Home telephone ____ - ____ - ______

I do wish to have my home address released to an □Yes

approved public employees’ organization. If left

unchecked, my address will not be released.

Have you applied to purchase all additional credit □Yes

for which you are eligible and intend to purchase? □No

Have you applied for credit for your active duty □Yes

military service? □No

Home email address: ___________________________________________

I request that my

retirement allowance

be effective on

Are you a U.S. citizen? □Yes □No

I have Voluntary Monies: (see instructions on page one)

□ I want my voluntary funds refunded in a one-time distribution.

OR

□ I want my voluntary funds to remain as a monthly additional annuity.

DESIGNATION OF BENEFICIARY:

NOTE: If more than one beneficiary

will be designated by members without a spouse or children under age 26 who select either the basic

allowance, the option 1 allowance, or the option 4 allowance, complete the “Designation of Beneficiary” Form 4 instead of the following

section. Retirees electing Option 2 or 5 cannot designate a beneficiary who is more than 10 years younger unless the beneficiary is the

retiree’s disabled child. □Check here to indicate that Form 4 is attached.

BENEFICIARY'S SOCIAL SECURITY NUMBER Gender DATE OF BIRTH

¯ ¯

RELATIONSHIP _____________________

¯ ¯

BENEFICIARY’S NAME (M or F) Month Day Year

First Initial Last

BENEFICIARY’S ADDRESS

Number and Street

City State ZIP Code

I hereby apply to retire from the Maryland State Retirement and Pension System (“SRPS”) and by signing below I confirm that:

1. REGARDING PAYMENT OF MY RETIREMENT BENEFIT, I authorize the Board of Trustees of the SRPS (“Board”) to pay to me and my properly designated

beneficiary or beneficiaries, according to the retirement allowance option I have chosen and my Designation of Beneficiary in this application. I agree on behalf of myself

and my heirs and assigns, that payment so made shall be a complete discharge of the claim and shall constitute a release of the Board and SRPS from any further

obligation concerning the benefit. I hereby direct that if each of my designated beneficiaries dies before me, the amount payable shall become a part of and be paid to

my estate, or to the beneficiary or beneficiaries I properly designate hereafter in accordance with the rules and regulations adopted by the Board.

2. REGARDING EACH OF MY BENEFICIARIES, I want the designation of beneficiary in this application to take effect (check only one box):

Immediately Only upon the effective date of my retirement

I understand that if I check neither box or both boxes, then the designation of beneficiary in this application will become effective immediately and will

replace all prior designation of beneficiary forms.

3. REGARDING REEMPLOYMENT,

I have read and understand the information about reemployment after retirement on pages two through four of this application. I

agree to notify the Board of my anticipated earnings if I return to work. I understand that exceeding the legal limit on my post-retirement earnings could cause a tempo-

rary reduction or termination of my monthly retirement allowance. I understand that, to retire, I must be separated from any and all employment and reemployment, of

any kind whatsoever, for at least 45 days after my retirement effective date, with any employer that participates in the SRPS. I also certify to the Board that at the date of

my retirement, I will be in compliance with that requirement, and that I have had no discussions about reemployment with any employer that participates in the SRPS.

4. REGARDING DEDUCTIONS FROM MY ALLOWANCE, if I elect to have any premiums, dues, or other expenses deducted from my allowance, I hereby authorize the

Maryland State Retirement Agency to exchange my Personal Information (including but not limited to my name, Social Security number and the amount of the

deductions) with the third party or parties receiving those premiums, dues, or other expenses.

You must sign and date this form in the presence of a Notary Public. Your application will be rejected and your retirement delayed

if the date of your s

ignature does not match the date of your appearance before the Notary Public as provided in the box below.

Complete Signature ________________ Date Signe

d _______

¯

¯

Page 9 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

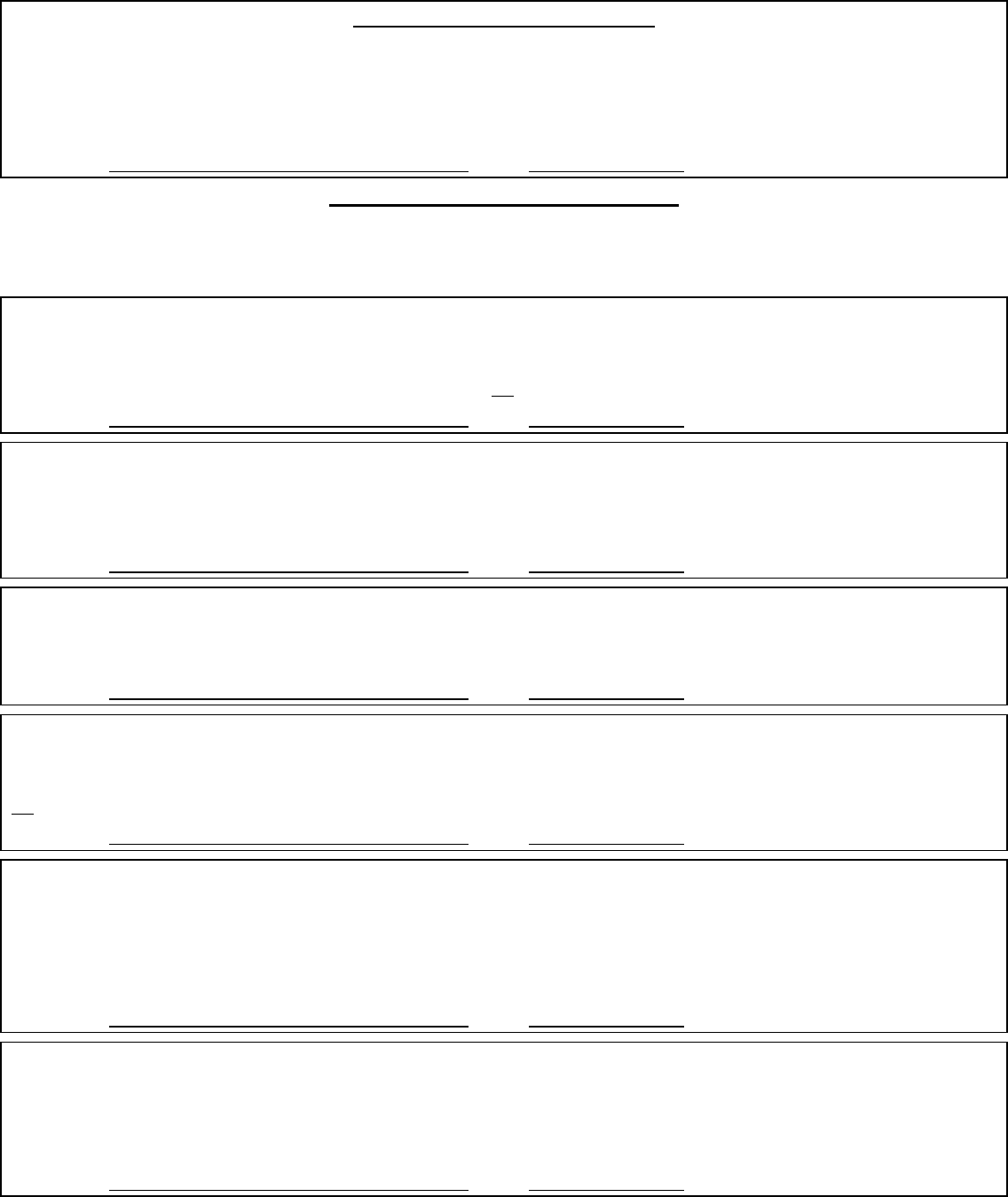

RETIREMENT ALLOWANCE OPTIONS

YOU MAY CHOOSE ONLY ONE OF THE FOLLOWING OPTIONS.

INDICATE YOUR SELECTION BY SIGNING IN THE APPROPRIATE BOX BELOW

BLOCK 1 - BASIC ALLOWANCE

The BASIC ALLOWANCE provides the largest allowance each month until your death. At your death, one-half of the monthly allowance will

be paid to your surviving spouse for life. If there is no eligible surviving spouse or if an eligible surviving spouse dies, then one-half of the

monthly allowance will be paid in equal shares to your children who are under age 26 until every child dies or attains age 26. If you have no

spouse or no children under age 26, the allowance ceases at your death and your beneficiary or estate will receive one payment if your death

occurs on the 16

th

of the month or later. If you die before the effective date of retirement, your selection shall be void and benefits due to the

death of a member in service will be paid. If you choose this option, you must send proof of your beneficiary’s date of birth with this application.

SIGNATURE DATE

BLOCK 2 - OPTIONAL ALLOWANCES

The following optional allowances are only available to members without a spouse as of the date of retirement. Sign the appropriate section

in this block to indicate the selected option. Optional allowances are effective on the effective date of retirement. If you die before the

effective date, the selected option shall be void and the benefits due to death of a member in service will be paid. The selected option

cannot be changed after the first payment normally becomes due.

OPTION 1:

Provides a lower monthly benefit than the Basic Allowance, but guarantees monthly payments that equal the total of your retirement

benefit’s Present Value. The Present Value of your benefit is figured at the time of your retirement. If you die before receiving monthly

payments that add up to the Present Value, the remaining payments will be paid in a lump sum to your designated beneficiary or

beneficiaries who remain alive. For state employees: Option 1 does not provide for continued health coverage after your death.

SIGNATURE DATE

OPTION 2:

Provides a lower monthly benefit than the Basic Allowance, but guarantees that after your death the same monthly benefit will continue to

be paid to your surviving beneficiary for his or her lifetime. No further payments will be made after the deaths of you and your beneficiary. If

you choose this option, you must send proof of your beneficiary’s date of birth with this application. Retirees electing Option 2 cannot

designate a beneficiary who is more than 10 years younger unless the beneficiary is the retiree’s disabled child.

SIGNATURE DATE

OPTION 3:

Provides a lower monthly benefit than the Basic Allowance, but guarantees that after your death one half of the monthly benefit paid to you

will be paid to your surviving beneficiary for his or her lifetime. No further payments will be made after the deaths of you and your

beneficiary. If you choose this option, you must send proof of your beneficiary’s date of birth with this application.

SIGNATURE DATE

OPTION 4:

Provides a lower monthly benefit than the Basic Allowance, but guarantees the return of your accumulated contributions and interest as

established when you retire. If you die before you have recovered the full amount of your accumulated contributions and interest, the

remainder will be paid in a lump sum to your designated beneficiary or beneficiaries who remain alive. For state employees: Option 4 does

not provide for continued health coverage after your death.

SIGNATURE DATE

OPTION 5:

Provides a lower monthly benefit than the Basic Allowance, but guarantees that after your death the same monthly benefit paid to you will

be paid to your surviving beneficiary for his or her lifetime. It also provides that your monthly benefit will “pop-up” to the Basic Allowance for

your lifetime the month following the death of your beneficiary if your beneficiary dies before you. If your original beneficiary dies and you

are collecting the Basic Allowance and decide to name a new beneficiary, your benefit will be recalculated under Option 5 based on the

new beneficiary designation. If you choose this option, you must send proof of your beneficiary’s date of birth with this application. Retirees

electing Option 5 cannot designate a beneficiary who is more than 10 years younger unless the beneficiary is the retiree’s disabled child.

SIGNATURE DATE

OPTION 6:

Provides a lower monthly benefit than the Basic Allowance, but guarantees that after your death one half of the monthly benefit paid to you

will be paid to your surviving beneficiary for his or her lifetime. It also provides that your monthly benefit will “pop-up” to the Basic Allowance

for your lifetime the month following the death of your beneficiary if your beneficiary dies before you. If your original beneficiary dies and

you are collecting the Basic Allowance and decide to name a new beneficiary, your benefit will be recalculated under Option 6 based on the

new beneficiary designation. If you choose this option, you must send proof of your beneficiary’s date of birth with this application.

SIGNATURE DATE

Page 10 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Month Day Year

APPLICATION FOR SERVICE OR DISABILITY RETIREMENT

To be completed by employer and returned with application

Employer’s Certification of Separation from Employment, Wages, Contributions and Sick Leave

For: ______________________________________________ __________________________________________

Applicant’s Name Job Classification

Applicant’s Social Security number:

A. The most recent payroll period reported was:

B. The projected payroll information to be reported prior to retirement is:

Contribution $ _____________ Standard hours _________ Actual Hours Paid _________ Pay Period Ending ___________________

MO DAY YR

Contribution $ _____________ Standard hours _________ Actual Hours Paid _________ Pay Period Ending ___________________

MO DAY YR

Contribution $ _____________ Standard hours _________ Actual Hours Paid _________ Pay Period Ending ___________________

MO DAY YR

Final

Contribution $____________ Standard hours _________ Actual Hours Paid _________ Pay Period Ending ___________________

MO DAY YR

No retirement contribution is due for a pay period ending on or after the retirement date.

C. The employee is separating from employment with the employer. The employee’s last day on payroll is: .

Federal law prohibits the Maryland State Retirement and Pension System from paying benefits prior to "separation from

employment." "Separation from employment" may only occur on resignation, retirement, discharge, or death, and not on

transfer, promotion, or otherwise continuing employment with the same employer without interruption. State law requires that

there be a minimum of 45 days from the date of retirement and the date the individual is reemployed, on a permanent,

temporary, or contractual basis, by: (a) the State or any other participating employer, or (b) a withdrawn participating

governmental unit (“PGU”), if the retiree was an employee of the withdrawn PGU while it was a participating employer.

D. Salary Change: Did the employee’s salary change since most recent payroll period reported or will

the employee’s salary change before the date of retirement?....................................................................

□YES □NO

If yes, the employee’s new annual salary is $ and is effective

MO DAY YR

E. Unused Sick Leave:

Member must retire within 30 days of separating from employment to be eligible to receive additional

creditable service for unused sick leave. The agency must be notified of all changes in unused sick leave. Unused sick leave

must be reported at the time the member files for retirement and again 30 days after the effective date of retirement.

Retirement Coordinator: Please retain a copy and submit recertified sick leave 30 days after retirement. Unused sick leave is

sick leave that was available to an employee as sick leave during employment and was not used before retirement. Any

converted leave that was not sick leave during employment may not be reported.

Initial

Reporting:

Total DAYS of unused sick leave (If none, enter word NONE) as of

MO DAY YR

Recertified

Sick

Leave:

Total DAYS of unused sick leave (If no change, enter no change) as of

MO DAY YR

Retirement Coordinator recertifying leave must initial here: Date: ______________

I certify that the above information regarding wages, contributions, separation from service, and sick leave is true and accurate

to the best of my knowledge and that I am authorized to certify this information by the employer. I will report any changes to

unused sick leave occurring between the date certified and the actual date of retirement.

_________________________________ _______________________________ _________________________________

Signature of Authorized Agent Printed Name of Authorized Agent Title of Authorized Agent

_________________________________ _______________________________ _________________________________

Date Full Name of Employer DIRECT Telephone Number

Submit form directly to: Maryland State Retirement and Pension System, 120 East Baltimore St., Baltimore, MD 21202-6700

-

¯

-

Page 11 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Deferred Retirement

Option Program

This page intentionally left blank

Page 12 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Page 1 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

SPECIAL TAX NOTICE REGARDING YOUR ROLLOVER OPTIONS

You are receiving this notice because all or a portion of a payment you are receiving from the Maryland State Retirement

and Pension System (the "Plan") is eligible to be rolled over to an IRA or an employer plan. This notice is intended to help

you decide whether to do such a rollover.

Rules that apply to most payments from a plan are described in the "General Information About Rollovers" section. Special

rules that only apply in certain circumstances are described in the "Special Rules and Options" section.

GENERAL INFORMATION ABOUT ROLLOVERS

How can a rollover affect my taxes?

You will be taxed on a payment from the Plan if you do not roll it over. If you are under age 59½ and do not do a rollover,

you will also have to pay a 10% additional income tax on early distributions (generally, distributions made before age 59½),

unless an exception applies. However, if you do a rollover, you will not have to pay tax until you receive payments later

and the 10% additional income tax will not apply if those payments are made after you are age 59½ (or if an exception to

the 10% additional income tax applies).

What types of retirement accounts and plans may accept my rollover?

You may roll over the payment to either an IRA (an individual retirement account or individual retirement annuity) or an

employer plan (a tax-qualified plan, section 403(b) plan, or governmental section 457(b) plan) that will accept the rollover.

The rules of the IRA or employer plan that holds the rollover will determine your investment options, fees, and rights to

payment from the IRA or employer plan. Further, the amount rolled over will become subject to the tax rules that apply to

the IRA or employer plan.

How do I do a rollover?

There are two ways to do a rollover. You can do either a direct rollover or a 60-day rollover.

If you do a direct rollover, the Plan will make the payment payable to your IRA or an employer plan for your benefit.

However, the payment may be mailed to you for delivery to your IRA or employer plan. You should contact the IRA sponsor

or the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit into an IRA or eligible employer plan that

will accept it. Generally, you will have 60 days after you receive the payment to make the deposit. If you do not do a direct

rollover, the Plan is required to withhold 20% of the payment for federal income taxes. In addition, the Plan is required to

withhold 7.75% for Maryland residents. This means that, in order to roll over the entire payment in a 60-day rollover, you

must use other funds to make up for the 20% withheld. If you do not roll over the entire amount of the payment, the portion

not rolled over will be taxed and will be subject to the 10% additional income tax on early distributions if you are under age

59 ½ (unless an exception applies).

How much may I roll over?

If you wish to do a rollover, you may roll over all or part of the amount eligible for rollover. Any payment from the Plan is

eligible for rollover, except:

• Certain payments spread over a period of at least 10 years or over your life or life expectancy (or the joint lives or

joint life expectancies of you and your beneficiary);

• Required minimum distributions after age 70½ (if you were born before July 1, 1949), after age 72 (if you were

born after June 30, 1949), or after death; and

• Corrective distributions of contributions that exceed tax law limitations.

The Plan administrator or the payor can tell you what portion of a payment is eligible for rollover.

Page 13 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Page 2 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

If I don't do a rollover, will I have to pay the 10% additional income tax on early distributions?

If you are under age 59½, you will have to pay the 10% additional income tax on early distributions for any payment from

the Plan (including amounts withheld for income tax) that you do not roll over, unless one of the exceptions listed below

applies. This tax applies to the part of the distribution that you must include in income and is in addition to the regular

income tax on the payment not rolled over.

The 10% additional income tax does not apply to the following payments from the Plan:

• Payments made after you separate from service if you will be at least age 55 in the year of the separation;

• Payments that start after you separate from service if paid at least annually in equal or close to equal amounts over

your life or life expectancy (or the joint lives or joint life expectancies of you and your beneficiary);

• Payments from a governmental plan made after you separate from service if you are a qualified public safety

employee and you will be at least age 50 in the year of the separation;

• Payments made due to disability;

• Payments after your death;

• Corrective distributions of contributions that exceed tax law limitations;

• Payments made directly to the government to satisfy a federal tax levy;

• Payments made under an eligible domestic relations order (EDRO) to an alternate payee who is a former spouse

of the member;

• Payments up to the amount of your deductible medical expenses (without regard to whether you itemize deductions

for the taxable year);

• Certain payments made while you are on active duty if you were a member of a reserve component called to duty

after September 11, 2001 for more than 179 days; and

• Payments excepted from the additional income tax by federal legislation relating to certain emergencies and

disasters.

If I do a rollover to an IRA, will the 10% additional income tax apply to early distributions from the IRA?

If you receive a payment from an IRA when you are under age 59 ½, you will have to pay the 10% additional income tax

on early distributions on the part of the distribution that you must include in income, unless an exception applies. In general,

the exceptions to the 10% additional income tax for early distributions from an IRA are the same as the exceptions listed

above for early distributions from a plan. However, there are a few differences for payments from an IRA, including:

• The exception for payments made after you separate from service if you will be at least age 55 in the year of the

separation (or age 50 for qualified public safety employees) does not apply;

• The exception for EDROs does not apply (although a special rule applies under which, as part of a divorce or

separation agreement, a tax-free transfer may be made directly to an IRA of a spouse or former spouse); and

• The exception for payments made at least annually in equal or close to equal amounts over a specified period applies

without regard to whether you have had a separation from service.

Additional ex

ceptions apply for payments from an IRA, including:

• Payments for qualified higher education expenses;

• Payments up to $10,000 used in a qualified first-time home purchase; and

• Payments for health insurance premiums after you have received unemployment compensation for 12 consecutive

weeks (or would have been eligible to receive unemployment compensation but for self-employed status).

Will I owe State income taxes?

If you do not do a rollover, the Plan is required to withhold 7.75% for Maryland residents. This notice does not address any

other State or local income tax rules (including withholding rules).

Page 14 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Page 3 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

SPECIAL RULES AND OPTIONS

If your payment includes after-tax contributions

After-tax contributions included in a payment are not taxed. If you receive a partial payment of your total benefit, an

allocable portion of your after-tax contributions is included in the payment, so you cannot take a payment of only after-tax

contributions. However, if you have pre-1987 after-tax contributions maintained in a separate account, a special rule may

apply to determine whether the after-tax contributions are included in the payment. In addition, special rules apply when

you do a rollover, as described below.

You may roll over to an IRA a payment that includes after-tax contributions through either a direct rollover or a 60-day

rollover. You must keep track of the aggregate amount of the after-tax contributions in all of your IRAs (in order to

determine your taxable income for later payments from the IRAs). If you do a direct rollover of only a portion of the amount

paid from the Plan and at the same time the rest is paid to you, the portion rolled over consists first of the amount that would

be taxable if not rolled over. For example, assume you are receiving a distribution of $12,000, of which $2,000 is after-tax

contributions. In this case, if you directly roll over $10,000 to an IRA that is not a Roth IRA, no amount is taxable because

the $2,000 amount not rolled over is treated as being after-tax contributions. If you do a direct rollover of the entire amount

paid from the Plan to two or more destinations at the same time, you can choose which destination receives the after-tax

contributions.

Similarly, if you do a 60-day rollover to an IRA of only a portion of a payment made to you, the portion rolled over consists

first of the amount that would be taxable if not rolled over. For example, assume you are receiving a distribution of $12,000,

of which $2,000 is after-tax contributions, and no part of the distribution is directly rolled over. In this case, if you roll over

$10,000 to an IRA that is not a Roth IRA in a 60-day rollover, no amount is taxable because the $2,000 amount not rolled

over is treated as being after-tax contributions.

You may roll over to an employer plan all of a payment that includes after-tax contributions, but only through a direct

rollover (and only if the receiving plan separately accounts for after-tax contributions and is not a governmental section

457(b) plan). You can do a 60-day rollover to an employer plan of part of a payment that includes after-tax contributions,

but only up to the amount of the payment that would be taxable if not rolled over.

If you miss the 60-day rollover deadline

Generally, the 60-day rollover deadline cannot be extended. However, the IRS has the limited authority to waive the deadline

under certain extraordinary circumstances, such as when external events prevented you from completing the rollover by the

60-day rollover deadline. Under certain circumstances, you may claim eligibility for a waiver of the 60-day rollover deadline

by making a written self-certification. Otherwise, to apply for a waiver from the IRS, you must file a private letter ruling

request with the IRS. Private letter ruling requests require the payment of a nonrefundable user fee. For more information,

see IRS Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs).

If you were born on or before January 1, 1936

If you were born on or before January 1, 1936 and receive a lump sum distribution that you do not roll over, special rules

for calculating the amount of the tax on the payment might apply to you. For more information, see IRS Publication 575,

Pension and Annuity Income.

If you are an eligible retired public safety officer and your payment is used to pay for health coverage or qualified

long-term care insurance

If you retired as a public safety officer, and your retirement was by reason of disability or was after normal retirement age,

you can exclude from your taxable income Plan payments paid directly as premiums to an accident or health plan (or a

qualified long-term care insurance contract) that your employer maintains for you, your spouse, or your dependents, up to

a maximum of $3,000 annually. For this purpose, a public safety officer is a law enforcement officer, firefighter, chaplain,

or member of a rescue squad or ambulance crew.

Page 15 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Page 4 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

If you roll over your payment to a Roth IRA

If you roll over a payment from the Plan to a Roth IRA, a special rule applies under which the amount of the payment rolled

over (reduced by any after-tax amounts) will be taxed. In general, the 10% additional income tax on early distributions will

not apply. However, if you take the amount rolled over out of the Roth IRA within the 5-year period that begins on January

1 of the year of the rollover, the 10% additional income tax will apply (unless an exception applies).

If you roll over the payment to a Roth IRA, later payments from the Roth IRA that are qualified distributions will not be

taxed (including earnings after the rollover). A qualified distribution from a Roth IRA is a payment made after you are age

59½ (or after your death or disability, or as a qualified first-time homebuyer distribution of up to $10,000) and after you

have had a Roth IRA for at least 5 years. In applying this 5-year rule, you count from January 1 of the year for which your

first contribution was made to a Roth IRA. Payments from the Roth IRA that are not qualified distributions will be taxed to

the extent of earnings after the rollover, including the 10% additional income tax on early distributions (unless an exception

applies). You do not have to take required minimum distributions from a Roth IRA during your lifetime. For more

information, see IRS Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs), and IRS Publication

590-B, Distributions from Individual Retirement Arrangements (IRAs).

If you are not a Plan member

Payments after death of the member. If you receive a distribution after the member’s death that you do not roll over, the

distribution generally will be taxed in the same manner described elsewhere in this notice. However, the 10% additional

income tax on early distributions and the special rules for public safety officers do not apply, and the special rule described

under the section "If you were born on or before January 1, 1936" applies only if the deceased member was born on or

before January 1, 1936.

If you are a surviving spouse. If you receive a payment from the Plan as the surviving spouse of a deceased member, you

have the same rollover options that the member would have had, as described elsewhere in this notice. In addition, if you

choose to do a rollover to an IRA, you may treat the IRA as your own or as an inherited IRA.

An IRA you treat as your own is treated like any other IRA of yours, so that payments made to you before you are age 59½

will be subject to the 10% additional income tax on early distributions (unless an exception applies) and required minimum

distributions from your IRA do not have to start until after you are age 70½ (if you were born before July 1, 1949) or age

72 (if you were born after June 30, 1949).

If you treat the IRA as an inherited IRA, payments from the IRA will not be subject to the 10% additional income tax on

early distributions. However, if the member had started taking required minimum distributions, you will have to receive

required minimum distributions from the inherited IRA. If the member had not started taking required minimum

distributions from the Plan, you will not have to start receiving required minimum distributions from the inherited IRA until

the year the member would have been age 70 ½ (if the participant was born before July 1, 1949) or age 72 (if the participant

was born after June 30, 1949).

If you are a surviving beneficiary other than a spouse. If you receive a payment from the Plan because of the member's

death and you are a designated beneficiary other than a surviving spouse, the only rollover option you have is to do a direct

rollover to an inherited IRA. Payments from the inherited IRA will not be subject to the 10% additional income tax on early

distributions. You will have to receive required minimum distributions from the inherited IRA.

Payments under an EDRO. If you are the spouse or former spouse of the member who receives a payment from the Plan

under an EDRO, you generally have the same options and the same tax treatment that the member would have (for example,

you may roll over the payment to your own IRA or an eligible employer plan that will accept it). However, payments under

the EDRO will not be subject to the 10% additional income tax on early distributions.

Page 16 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Page 5 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

If you are a nonresident alien

If you are a nonresident alien and you do not do a direct rollover to a U.S. IRA or U.S. employer plan, instead of withholding

20%, the Plan is generally required to withhold 30% of the payment for federal income taxes. If the amount withheld exceeds

the amount of tax you owe (as may happen if you do a 60-day rollover), you may request an income tax refund by filing

Form 1040NR and attaching your Form 1042-S. See Form W-8BEN for claiming that you are entitled to a reduced rate of

withholding under an income tax treaty. For more information, see also IRS Publication 519, U.S. Tax Guide for Aliens,

and IRS Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities.

Other special rules

If a payment is one in a series of payments for less than 10 years, your choice whether to do a direct rollover will apply to

all later payments in the series (unless you make a different choice for later payments).

If your payments for the year are less than $200, the Plan is not required to allow you to do a direct rollover and is not

required to withhold federal income taxes. However, you may do a 60-day rollover.

You may have special rollover rights if you recently served in the U.S. Armed Forces. For more information on special

rollover rights related to the U.S. Armed Forces, see IRS Publication 3, Armed Forces' Tax Guide. You also may have

special rollover rights if you were affected by a federally declared disaster (or similar event), or if you received a distribution

on account of a disaster. For more information on special rollover rights related to disaster relief, see the IRS website at

www.irs.gov.

FOR MORE INFORMATION

You may wish to consult with the Plan administrator or a professional tax advisor, before taking a payment from the Plan.

Also, you can find more detailed information on the federal tax treatment of payments from employer plans in: IRS Publi-

cation 575, Pension and Annuity Income; IRS Publication 590-A, Contributions to Individual Retirement Arrangements

(IRAs); IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs); and IRS Publication 571,

Tax-Sheltered Annuity Plans (403(b) Plans). These publications are available from a local IRS office, on the web at

www.irs.gov, or by calling 1-800-TAX-FORM.

The State Retirement Agency strongly urges you to consult with a qualified tax advisor, the Internal Revenue Ser-

vice, or a Certified Public Accountant regarding the tax consequences of your distribution as it relates to your spe-

cific tax situation.

Page 17 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

Deferred Retirement

Option Program

This page intentionally left blank

Page 18 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

MARYLAND STATE RETIREMENT AGENCY

120 EAST BALTIMORE STREET

BALTIMORE, MD 21202-6700

APPLICATION FOR THE DEFERRED

RETIREMENT OPTION PROGRAM (DROP)

LAW ENFORCEMENT OFFICERS’ PENSION SYSTEM (LEOPS)

RETIREMENT

USE ONLY FORM 504 (REV. 7/23)

Important: Print in ink or type all entries except for signatures. Complete all sections of the application. Contact a Retirement Benefits

Specialist at 410-625-5555 or toll-free at 1-800-492-5909 for assistance.

SECTION I - MEMBER INFORMATION

APPLICANT’S SOCIAL SECURITY NUMBER

DAYTIME TELEPHONE

- -

APPLICANT’S NAME

First Initial Last

HOME ADDRESS

Number and Street

-

City State ZIP Code

APPLICANT’S DATE OF BIRTH E-MAIL ADDRESS

- -

Month Day Year

SECTION II - ELECTION TO PARTICIPATE; EFFECTIVE DATE OF PARTICIPATION

I hereby elect to participate in the Deferred Retirement Option Program (DROP)

for members of the Law Enforcement Officers’ Pension System effective on the first day of

Month Year

DROP PARTICIPATION PERIOD:

My DROP participation shall begin on the effective date specified above and shall continue for a period not to exceed the lesser of (check

applicable period):

7 years

Difference between 32 years and my creditable service as of the date of my election to participate in the

DROP

Specific number of years and months (which may not exceed 7 years)

ENDING DATE OF DROP PARTICIPATION PERIOD:

My DROP participation shall end on

Month Day Year

which is the date I intend to separate from employment with my employer as evidenced by the binding letter of resignation that I have

submitted to my employer and that is attached to this Application. My period of DROP participation will end before the date specified

above if one of the following events occur: (1) my death; (2) my termination from employment by my employer for any reason before the

date specified; or (3) my acceptance of an accidental disability retirement allowance.

EFFECT OF TERMINATION OF DROP PARTICIPATION PERIOD:

On the ending date of my DROP participation period, I intend to terminate my employment with my employer. The Agency shall begin

paying a retirement allowance to me based on my creditable service and average final compensation as of the effective date of my

participation in the DROP, increased by any cost of living adjustments payable during the DROP participation period. In addition, within

90 days after receipt of my Application for Withdrawal of DROP Account (SRA Form 505) and any other information that the State

Retirement Agency requires to process the withdrawal, the Agency shall pay me (or my allowable designee) the amount accrued in the

DROP for my benefit.

Continued on following page

FORM 504 (REV. 7/23) Page 1 of 2

-

- -

Page 19 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

ACKNOWLEDGMENTS:

By submitting this application, I hereby acknowledge and certify, as follows:

(1) Understand the DROP. I have carefully reviewed the summary of the terms of the DROP and Section 26.401.1 of the Annotated

Code of Maryland regarding the DROP. I have discussed any questions I have about retirement benefits payable under the DROP and

the Law Enforcement Officers’ Pension System with a retirement benefits specialist at the Maryland State Retirement Agency.

(2) Irrevocable Election. My election to participate in the DROP is irrevocable.

(3) Retiree. As of the effective date of my DROP participation, I have retired from the Law Enforcement Officers’ Pension System,

and therefore, during my DROP participation period, I will not earn any additional service credits in, or make member contributions to the

Law Enforcement Officers’ Pension System. Nor will any increases in salary affect my Average Final Compensation.

(4) Agency Acceptance of Application. My election to participate in the DROP will not be accepted by the State Retirement Agency

if I do not: (a) satisfy the eligibility requirements for the DROP specified in the Annotated Code of Maryland, section 26.401.1; or (b)

submit the required attachments specified in Section III of this Application. The Agency shall notify me promptly if my application is not

accepted.

(5) Agency Audit of Retirement Account. The period of my participation in the DROP is subject to adjustment by the State

Retirement Agency on audit of my retirement account. If the Agency makes any adjustments to my retirement account that affects my

participation in the DROP, including the duration of my participation in the DROP, I understand that the Agency will notify me of the

adjustment and I agree to promptly submit to the Agency a revised application to participate in the DROP.

(6) Unused Sick Leave. As of the effective date of my participation in the DROP, the Agency computed my normal service retirement

allowance, granting me creditable service for my unused sick leave as provided in '20-206 of the Pension Article, Annotated Code of

Maryland. If, at the end of my DROP participation period, I have any unused sick leave, I will not receive any additional creditable service

and my retirement allowance will not be adjusted.

(7) Beneficiary. If I die before the end of the DROP participation period, the balance in my DROP account shall be payable as follows:

(a) to my surviving spouse;

(b) if I am not survived by my spouse, in equal shares to my children who have not attained age 26;

(c) if I am not survived by my spouse or any child who is under age 26, to the person named as the beneficiary of my retirement

allowance on the Application For Service Retirement (SRA Form 98) submitted with this application; or

(d) if the person designated as the beneficiary of my retirement allowance on the SRA Form 98 is not living, to my estate.

(8) Voluntary Funds. I understand that participation in the DROP precludes me from withdrawing my voluntary funds, if any. The

State Retirement Agency shall pay my voluntary money as an additional annuity over my lifetime (if applicable).

(9) Accidental Disability Retirement. I understand that as a DROP member I am eligible for line of duty (accidental) disability benefits

only if I am totally and permanently incapacitated for duty as a result of an accident or condition that arises out of or in the course of the

actual performance of duty during my participation in the DROP, and without willful negligence on my part.

(10) Rollover Options (“Special Tax Notice”). I have had an opportunity to review the Special Tax Notice with my tax advisor,

accountant, attorney, or the IRS, and understand my options with respect to receipt of a distribution from the System at this time. I

understand that I have at least 30 days to review the Special Tax Notice and consider whether or not to have my payment rolled over. I

further understand that, if I complete and submit this form prior to the end of the 30-day period for reviewing the Special Tax Notice, I

have waived my right to the 30-day period to review the Special Tax Notice.

(11) Interest. DROP accounts receive 4% interest compounded annually. Interest is calculated based on the beginning balance (2%)

and the ending balance (2%) and is calculated at fiscal year end, June 30 or at termination.

SECTION III C REQUIRED ATTACHMENTS: Attached to this application are the following:

(1) Application For Service Retirement (SRA Form 98) and

(2) Binding Letter of Resignation (SRA Form 507) accepted by the Secretary of your Department or the Secretary’s designee

reflecting termination of my employment with my employer on the ending date of my DROP participation period

SECTION IV

Applicant’s Signature Date

Retirement Coordinator Signature Date

FORM 504 (REV. 7/23) Page 2 of 2

Page 20 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)

MARYLAND STATE RETIREMENT AGENCY

120 EAST BALTIMORE STREET

BALTIMORE, MD 21202-6700

BINDING LETTER OF RESIGNATION

DEFERRED RETIREMENT OPTION PROGRAM (DROP)

LAW ENFORCEMENT OFFICERS’ PENSION SYSTEM (LEOPS)

FOR RETIREMENT

USE ONLY FORM 507 (REV. 8/19)

Important: Print in ink or type all entries except for signatures. Complete all sections. Contact a Retirement Benefits

Specialist at 410-625-5555 or toll-free at 1-800-492-5909 for assistance.

SOCIAL SECURITY NUMBER

DAYTIME TELEPHONE NUMBER

- -

NAME

First Initial Last

HOME ADDRESS

Number and Street

-

City State ZIP Code

EMAIL ADDRESS

Pursuant to State Personnel and Pensions Article, §26-401.1 (e) (1) (i) 4, I hereby elect to participate in the

Deferred Retirement Option Program (DROP). I have completed the following forms as a requirement of

participation:

Application for the Deferred Retirement Option Program (Form 504)

Application for Service or Disability Retirement (Form 98-101)

I will begin participation in the Deferred Retirement Option Program effective

Month Day Year

My DROP termination date will be

Month Day Year

I understand that my election to participate in the DROP is irrevocable.

I have read and understood the rules and regulations pertaining to all aspects of the DROP and fully accept

these conditions by signing and submitting this Binding Letter of Resignation.

Applicant’s Signature: _______________________________ Date: ____________

Retirement Coordinator Signature: _______________________________ Date: ____________

-

-

-

-

Page 21 of 21

Law Enforcement Officers' Pension System Deferred Retirement Option Program (DROP) Enrollment Package (REV. 7/23)